19th of May 2009: Hawkins Wright has published the first report about Forest Energy - The Forest Energy Monitor (Text from archive for![]() Download, 1.8 MB).

Download, 1.8 MB).

It's quite interesting what the consultancy has discovered so far:

Pulpwood is normally outside the reach of energy buyers, but with demand from traditional end-users falling, prices of pulpwood have dropped to levels barely higher than those of energy wood. Consequently, in Sweden for example, pulpwood is now being chipped for energy uses, either for heat and power or pellts. The same is true elsewhere, although in some areas the trend has been delayed by the need for investment in equipment to chip and process logs rather than residues. In many cases these investments are now under way, although inevitably they will push up costs. The growth in energy wood demand is therefore changing the nature of pulpwood and chip markets, with important implications for the traditional forest industries. These are permanent changes that will not simply be reversed when pulp, paper and sawn timber demand recovers. Energy wood is creating a floor beneath the pulpwood market, and given the scale of our governments’ renewable energy targets – and the need to mobilize more costly sources of energy wood – it is a foor that is far more likely to rise than to fall in the future. This will eventually place upward pressure on pulpwood prices and increase the competition between energy and traditional pulpwood buyers.

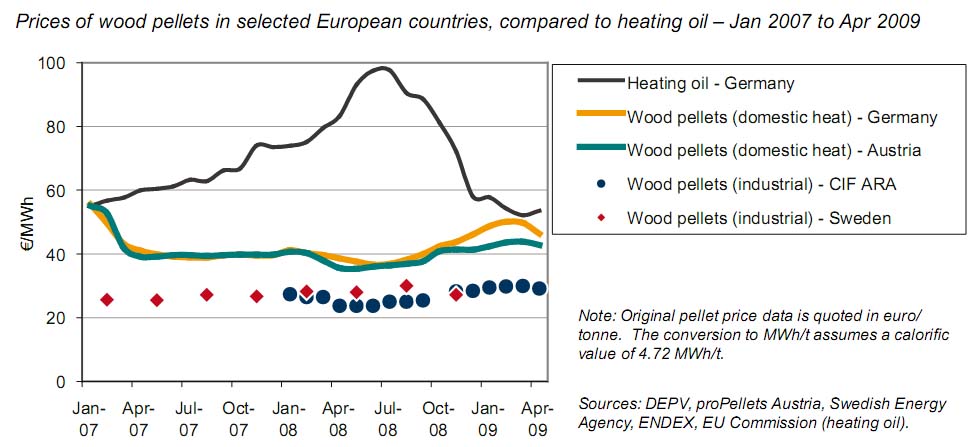

For ilustration purpose just an interesting graph:

Just curious on how national policies of European countries will act on those new developments...

If you want to read more about global timber markets and wood prices, just follow this link

WRI - Wood Resource Quarterly: Wood fiber costs are rising for wood pellets manufacturers in Europe because the industry is expanding rapidly

WEBWIRE – Friday, May 29, 2009

The expanding wood pellet industry in Europe is increasingly relying on pulpwood and wood chips for its raw-material needs, as the supply of lower-cost sawdust cannot meet the fast rise in demand for wood fiber. The biomass sector is now competing with both the wood-based panel manufacturers and pulpmills for wood residues and logs, reports the Wood Resource Quarterly.

Seattle, USA. June 2009. The competition for wood raw-material in Europe has been intensifying the past few years as sawmills, wood-panel manufacturers, pulpmills and bio-energy facilities expanded capacity during 2006 and 2007 and therefore increased the usage of roundwood and wood residues. Lately, the pulp market has weakened resulting in lower demand and prices for pulpwood in all countries in Europe. However, the decline has been less pronounced in markets where the pellet industry has a strong presence.

The increased demand for biomass from the energy sector has not only had an impact on prices of residual chips from sawmills (wood chips, sawdust and shavings) but also of small-diameter logs, which have increasingly been utilized for energy generation. These developments have been particularly prominent in Germany and Sweden the past year. In Germany, prices for sawdust, wood chips and hardwood logs have converged during 2008 and 2009, and were in the first quarter practically the same (measured in dry tons), as reported in the Wood Resource Quarterly.

In Sweden, small logs that would typically go to pulpmills have in recent months been sold to energy plants. With the demand and prices for pulpwood being in decline and the consumption of “energy wood” steadily rising, competition for smaller logs has intensified and it is expected that volumes of wood chips and logs bound for energy facilities will increase, thus potentially decreasing that going to pulpmills in the future. The rise in demand for forest biomass, including branches, stumps and tops will encourage more intensive management schemes with higher utilization of the forest resources not only in Sweden but in the rest of Europe as well.

With the energy sector emerging as a new and aggressive market player, floor prices for wood chips and pulplogs are not expected to ever return to the low levels of the late 1990’s again. The increased competition for raw-material between the biomass sector, the composite board manufacturers and the pulp industry will result in relatively high fiber costs even in weak markets for forest products in the future. The recent evolution of the wood raw-material market in Europe is not unique to this continent but can be expected to take place in North America as well in the coming years.

Global timber market reporting is included in the 50-page publication Wood Resource Quarterly. The report, established in 1988 and with readers in over 25 countries, tracks wood chips and pulpwood prices in most regions around the world and also includes regular updates of the latest developments in international timber, pulp, lumber and biomass markets.

Contact Information

Wood Resources International LLC

Hakan Ekstrom

info@wri-ltd.com

---------------

Energy wood prices at same level as pulpwood prices